The accounting industry is changing, majorly due to never-ending development in technology and its uses in accounting practices. Technology in accountancy (with proper utilization) is leading to quicker completion of accounting operations with precise numbers. Thus, let’s first discuss the technologies impacting accounting practices and CPA firms:

Artificial Intelligence & Robotics:

AI and RPA (robotic process automation) are automating repetitive and complex accounting processes, with high accuracy, increasing operational efficiency, and cutting costs. Apart from these, the use of these technologies in CPA firms also saves a significant amount of accountants’ time.

Cloud Computing:

Cloud computing is the concept of internet-based computing that allows accountants to manage accounting functions from any place. Cloud also helps accountants to provide clients with financial data and reports through the internet, reducing the use of paper and saving costs.

Blockchain:

Blockchain technology offers authorized users access to a secure transaction ledger. A recent report by Deloitte speculated that the long-established double ledger accounting system could potentially be replaced by blockchain by allowing accountants to enter transactions on a register where entries could only be changed by users with a permit to do so.

Tax Software:

CPA firms that prepare taxes for their clients as a part of complete business accounting services are taking help from tax software in achieving up to the mark accuracy in tax preparation. All of this helps their clients prevent penalties and issues with stakeholders. As a result, they are becoming capable of delivering quality services and making clients happily satisfied.

E-Signature:

CPA firms usually deal with an abundance of documents. But with eSignature solutions, they are reducing the heaps of paperwork. Most signature transactions are likely to be processed on mobile devices in the future, which will also be better for clients’ convenience.

The Actual Impact of Technologies:

- Effortless Bookkeeping:

Traditional bookkeeping practices always require accountants’ complete attention and are undoubtedly time-consuming. However, these days, automated data entry & categorization is helping CPA firms manage the exhausting, daily bookkeeping tasks efficiently. CPAs can invest the time saved (due to automation) on enhancing their knowledge base.

- Better Expense Management

It takes a lot of time to review and approve all the company expenses in order to ensure they don’t breach the company’s policies. Technologies like AI are making it easier to check receipts of purchase, review expenses while making sure they are compliant with the policies of the company.

- Increased Audit Quality:

AI platforms will be a boon for auditors throughout the world. It will enhance not only efficiency but also quality in auditing while providing more insights. It also helps to inspect data in more depth and delivers clean data for further use.

Current scenario:

58% of large-size companies are already using cloud accounting (Accounting Today)

50% of labor costs are reduced by cloud computing (Forbes)

78% of small-size businesses are likely to rely solely on cloud solutions by the end of 2024 (Accountancy Age)

The global market of accounting is expected to reach $4.25 billion by 2024 which recently was $2.62 billion (AB Newswire)

More than 80% of executives believe artificial intelligence gives their company a competitive advantage, while 79% expect it will boost their company’s productivity. (Journal of Accountancy)

RPA, short for robotic process automation, has reduced turnaround time for contractual processing & audit from many months to just a few weeks. (Forbes)

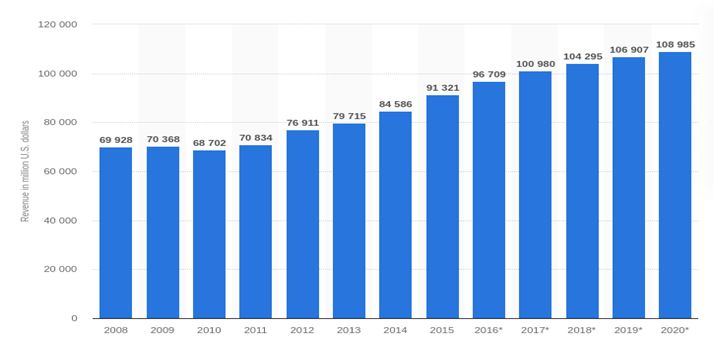

Revenue of U.S. CPA firms from 2008 to 2024

What Could Happen If You Don’t Opt for Technologies Your CPA Firm Requires?

Your Requirements Might Drain Your Budget

As your firm will grow with time, you will get more clients, more work, and the same will go on. Not using technology (accounting software) might take a toll on your budget, as you would spend more on hiring more accountants to manage your clients’ accounting and satisfy them with your services. A full-time accountant’s average salary is more than $70,000 a year.

Lack of Security

Keeping records in basic accounting programs on your computers might put your and your clients’ highly confidential financial data at risk. Without a secure & reliable software application, the data sets containing your clients’ names, bank & credit card details are prone to cyber theft.

Possibility of Errors

Manual accounting processes are more likely to have errors. For example, entering 23 instead of 32 is a common typographical error and can make the entire balance sheet unbalanced, leading to inaccurate financial reporting. Thus, a lack of technology (automated accounting applications) can make your firm spend more time on reconciliations.

Your Firm Will Lag Behind

The future of accounting is most likely to depend upon technology. “More than a third of accountants surveyed (35%) regard their firms as early adopters of technology, investing readily in the best technology available in order to stay ahead of competitors and diversify their offerings.”, according to Sage.

Technology Trends that Should not be Ignored

- Communication Tools

Accountants generally don’t use social media or allow their clients to have a conversation on the text. But they communicate through emails because most clients prefer to have a personalized medium of contact to reach their accountants. As the next generation of entrepreneurs and business owners will find texting as the most convenient way to communicate, your CPA firm should offer multiple contact channels to clients.

- Remote Data Accessibility

The new era CPA firms have already started utilizing remote technologies. Today firms want their accountants to meet clients personally or work from home when required. With the help of remote access, accountants can visit their clients and access data in their office that was prepared at their firm. For how long will they carry paper stacks?

- Data Security

People are using the internet for a few decades now, saving their confidential information on the internet and even making payments online. We all were told that the internet is safe, and it keeps your data secure. Well, quite the contrary, some of the largest companies like Uber, eBay, TJX Companies, Inc., Adobe, Sony (Playstation Network), including the internet giant – Yahoo and one US federal agency – OPM had been the victim of some of the biggest data breaches in the history of the internet. Your clients want reassurance that their confidential data which includes their bank and credit card information is safe with you. Thus, you need to adopt top security measures to secure the data online.

- Online Filing

The IRS offers a pilot online filing program that taxpayers are using since 1986. In 2017, more than 152 million returns were processed, out of which 132,319,000 were submitted using eFile, where tax professionals submitted around 60% of tax returns. CPAs should take advantage of technology rather than being in fear of getting replaced by it.

- The Cloud

Clients are concerned about their files in your office or data in your computers getting lost or taken away by floods and tsunamis. They want to be sure that their information (which they have been maintaining for years) is recoverable in case of emergencies like a fire, earthquake, typhoon, etc., hit your office. CPAs should not ignore cloud solutions and adopt them for data storage and accounting practices.

Future of CPA firms:

Technology will have a massive impact on CPA firms, making them develop their roles, especially as a consultant. Clients will expect their CPAs to deliver future-oriented services, for example, insights into the current status and forecasts of their business financials. Technologies such as AI, robotics, and machine learning have already started to reduce the time CPAs spend on tax compliance and audits. As accountants will save a lot of time, they might invest it in building strategies to improve their services to achieve client satisfaction.

Klassen Jamjoum (vice president in Kearney’s Digital Center of Excellence) says, “In a future where we are increasingly surrounded by AI, we will crave human interaction even more.””And many jobs will be augmented by AI, meaning people can achieve things they never thought possible. Technology should empower, not take away.”

Conclusion:

It’s a misconception that technology will replace accountants; in fact, technologies discussed above should be taken as an opportunity. For CPA firms, offering add-on services such as strategic financial planning or advising ensures higher value is being delivered to clients, and they can make and maintain meaningful client-firm relationships.

Apart from accountancy, technology will not only have an impact on how you communicate with clients but also how you conduct and manage your CPA firm’s internal operations. When you strategically implement new technology, your expenses for that will become an investment that can boost your firm’s efficiency, productivity, and credibility.

However, it is common for CPAs and CPA firms to remain busy throughout the year, but the load of work frequently fluctuates. Many firms take their own unique decisions and ways to tackle this challenge. For some, outsourcing is a better option than investing in technologies, while some adopt technologies to improve productivity.

As technology might soon replace manual, time-consuming calculations, it will be better to use the time saved in reaping all possible benefits of adopting cloud, AI, and robotics-based accounting applications for a better, successful, and client-oriented future of your CPA firm.

Tracy Watson works as an Accounting Expert at Accounting To Taxes, a renowned company offering Tax, Financial, and Accounting Outsourcing Services. She is passionate about writing about finance & accounting, small business growth, and entrepreneurship. She is continuously contributing her skills, knowledge, and experience in assisting people with finance and accounting matters.